News

What is discount rate? Role, calculation method and 5+ influencing factors

![]() 11/11/2025

11/11/2025

Have you ever heard of the concept?What is the discount rate?but do not clearly understand its role and impact on the economy? This is one of the important tools that helps the State Bank manage monetary policy, directly affecting the cost of capital, credit and economic growth in the market.

1. Overview of discount rates

1.1. Concept

Concept of discount rate is defined differently depending on the field:

- In corporate finance: Discount rate used to convert future cash flows to the present.

- In the banking system: Discount rate is the interest rate applied by the State Bank when lending to commercial banks for refinancing through the discounting of valuable papers.

Discount rates are calculated using several methods such asNPV (Net Present Value), IRR (Internal Rate of Return), WACC (Weighted Average Cost of Capital),..., depending on the purpose of use (investment, borrowing, project appraisal,...) and the specific economic context.

Discount rates are commonly used in the following areas:

- Asset and securities valuation.

- Analysis and evaluation of investment efficiency.

- Financial risk management.

- Long-term financial planning

Discount rates are applied in a variety of fields.

1.2. Role

The discount rate is not only an important financial tool in banking operations but also a lever for macroeconomic regulation of the economy. Depending on the policy objective, this interest rate can be adjusted to control inflation, stabilize currency or support economic growth.

For commercial banks:

- It is a tool to mobilize short-term capital when needing to borrow from the State Bank (SBV).

- Helps maintain liquidity, ensures solvency and stable operations.

- Yesc affects the interest rate level of mobilization and commercial lending.

For the State Bank:

- As a key monetary policy tool, it helps control money supply in the economy.

- By increasing the discount rate, the State Bank limits borrowing from banks, reducing the amount of money in circulation to control inflation.

- By lowering the discount rate, banks are encouraged to borrow more, stimulating investment and economic growth.

2. Operating mechanism and impact of discount rate

2.1. Operating mechanism of discount transaction

In banking operations, discounting is the process by which commercial banks (CBs) resell valuable papers such as bills of exchange, treasury bills or bonds to the State Bank (SBV) to receive cash before maturity.

The process goes like this:

- Step 1:Commercial banks submit valuable papers to the State Bank along with the discount request file.

- Step 2: The State Bank reviews the validity and decides to discount at the current discount rate.

- Step 3: The commercial bank receives cash after deducting the discount – this is a short-term secured loan.

Discount operations play an important role in maintaining the liquidity and stability of the banking system. For commercial banks, this is an effective short-term solution to supplement working capital when there is a temporary shortage of cash without having to mobilize from the market.

Discount operations maintain liquidity and stability of the banking system.

For the State Bank, this operation is a tool to regulate monetary policy, helping to control money supply, stabilize interest rates and support liquidity balance in the entire financial system.

2.2. Impact of changes in discount rates

Adjusting the discount rate (LSCK) is one of the important monetary policy management tools of the State Bank (SBV). When the SBV increases the LSCK, the borrowing costs of commercial banks (CBs) increase, leading to an increase in lending interest rates in the market, thereby limiting credit activities and contributing to curbing inflation. On the contrary, when the SBV reduces the LSCK, the borrowing costs of commercial banks decrease, causing lending interest rates to tend to decrease, thereby promoting borrowing activities, expanding credit and stimulating economic growth.

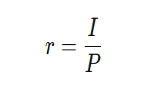

3. Formula for calculating discount rate

3.1. Cost of capital mobilization

This is an interest rate determined based on the cost that banks or businesses have to pay to raise capital, often used to price investments or financial projects.

Recipe:

In there:

- r: Discount rate

- I: Cost of capital mobilization (interest payable)

- P: Amount of capital mobilized

For example:If a business raises 1 billion VND and has to pay 100 million VND in interest, the discount rate is:r=100.000.000/1.000.000.000=10%

3.2. Weighted average cost of capital

This is the interest rate that reflects the average cost of capital that a business must bear from various sources such as loans, equity, or bonds. WACC is often used in the valuation of businesses or investment projects.

Recipe:

In there:

- AND: Equity value

- D: Loan value

- In: Total capital value (E + D)

- Re: Cost of equity

- Rd: Cost of debt

- TCorporate income tax rate

For example:A company has 60% equity at 12% cost and 40% debt at 8% cost, tax rate 20%.

→ The weighted average discount rate of the business is9,44%.

4. 4 Important factors affecting discount rates

The discount rate is not fixed but fluctuates according to many economic and financial factors, reflecting the relationship between monetary policy, inflation and market conditions. Below are the main factors that affect this interest rate:

- Inflationary: When the inflation rate increases, the value of money decreases, causing the State Bank to tend to raise the discount rate to control the amount of money in circulation and curb inflation.

- Supply and demand of capital in the market: When the demand for loans increases or the money supply decreases, the discount rate usually increases because the cost of raising capital is higher. Conversely, when the money supply is abundant, the discount rate tends to decrease.

- Monetary policy: This is the most direct factor. When the State Bank wants to stimulate the economy, it reduces the discount rate; when it needs to control inflation or reduce risky credit, the State Bank will increase this interest rate.

- Term and credit risk: Long-term or high-risk loans typically carry higher discount rates to compensate for the risk of future capital loss and market volatility.

Inflation is one of the factors affecting discount rates.

5. Frequently Asked Questions

1. Who is eligible for discount loans?

Only commercial banks or credit institutions are allowed to borrow from the State Bank (SBV) at discount rates to supplement short-term liquidity.

2. Is the discount rate the same as the normal lending rate?

No. Discount interest rates apply between the State Bank and commercial banks, while normal lending interest rates apply between banks and individual/corporate customers.

3. Does a change in the discount rate directly affect my deposit interest rate?

There is an indirect impact. When the State Bank adjusts the discount rate, banks will consider adjusting their deposit and lending rates to match the general interest rate level in the market.

6. Save money and borrow money with preferential interest rates at SeABank

If you are looking for a financial solution with preferential interest rates, quick procedures, and transparent services, SeABank is a reliable choice. Here, you can both deposit savings with attractive interest rates and easily borrow capital to suit your personal and business needs.

- Savings deposit: SeABank offers savings programs with attractive interest rates, especially when you deposit via SeAMobile or SeANet, with many flexible terms from short to long.

- Loan: Diversified with unsecured loan products, mortgage loans or business loans. ProceduresAt SeABank, it's simple, quick approval with competitive interest rates - helping you access capital safely and legally.

Contact SeABank today to get advice on the latest interest rates and choose a savings or loan package that suits your financial goals.

Clearly understanding What is the discount rate? not only helps you grasp the trend of currency management but also supports in predicting fluctuations in market interest rates. If you are looking for a safe financial solution, SeABank offers loan - savings packages with preferential and transparent interest rates.

If you want to learn more about SeABank's card products, you can contact the nearest transaction point or call Hotline 1900 555 587 or visit the website www.seabank.com.vn for more details.