Compound interest - formula, examples, applications and important notes

11/11/2025

Refer to the article now to discover the detailed compound interest calculation formula, helping you optimize profits and effectively manage your investments or savings.

Compound interest is a form of interest calculation where the interest generated is added to the principal to continue generating interest in the following periods. This is considered the "8th wonder of the world" because of its power to double assets over time. Understanding and applying the compound interest formula helps each person optimize savings, investments and long-term financial development.

Note: The figures and information in the article are compiled from general market sources and do not apply specifically to SeABank's products or services.

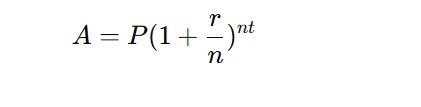

1. Basic compound interest formula

General formula:

In there:

A: Final amount after investment/saving period

P: Initial principal

r: Annual interest rate (in decimal form, e.g. 8% = 0.08)

n: Number of times interest is compounded in a year (e.g. 12 times if calculated monthly)

t:Number of years to deposit or invest

For example: You deposit 100 million VND with an interest rate of 8%/year, compounded once a year for 5 years:

A = 100,000,000 × (1 + 0.08)^5= 146,932,807

→ After 5 years, the value of the amount will be approximately 146.9 million VND..

Understanding the compound interest formula helps optimize the savings process.

2. Variations of the compound interest formula

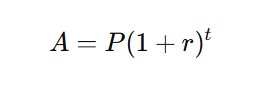

2.1. Annual compound interest

Annual compound interest is a form of interest calculation where the entire interest of the previous year is added to the principal, and the interest of the following year continues to be calculated on the new total (principal + interest). This is the most common form in savings or long-term investments.

Recipe:

In there:

P: initial principal amount

r: annual interest rate (in decimal form)

t: number of years to deposit or invest

For example: You deposit 50 million VND, interest rate 10%/year for 3 years:

→ A = 50,000,000 × (1 + 0.1)^3 = 66,550,000

The annual compound interest formula is applied when you deposit savings or invest for a term of 1 year or more and commit to not withdrawing money in the middle. This formula is suitable for products such as:

Long-term savings

Bonds

Investment funds, or investments that reinvest profits annually.

Typically, this method of compounding interest is simple and suitable for long-term financial goals because profits increase exponentially. However, products that use this method often require long-term commitments and are difficult to withdraw money flexibly.

2.2. Compound interest monthly or quarterly

In this case, interest is compounded multiple times a year — monthly or quarterly. The more times interest is compounded, the higher the total interest received because the interest “earns interest” more often.

This formula is applied when a bank or financial institution offers a savings product that calculates interest and compounds it over a period of less than a year (monthly or quarterly). Therefore, monthly/quarterly compounding is often found in flexible savings products, automatic savings accounts, or recurring deposit programs.

Recipe:

In there:

P is the initial principal amount

r is the annual interest rate in decimal form

nis the number of compounding times in a year

By month:n = 12

Quarterly:n = 4

t is the number of years of deposit or investment

For example: You deposit 100 million VND, interest rate 12%/year, compounded monthly (n = 12), for 1 year:

→ A = 100,000,000 ×(1 + 0.12/12)^12 = 112,682,500

It can be seen that this calculation method has a higher profit margin than annual compounding (with the same interest rate), however, the formula is often more complicated, some banks apply stricter binding conditions in deposit products.

2.3. Compound interest with additional recurring deposits

This is a form of both initial deposit and periodic top-up (monthly/quarterly). This form is suitable for those who want to save regularly and take advantage of the power of long-term compound interest.

Recipe:

In there:

P: initial principal amount

r: annual interest rate (in decimal form)

n: number of compounding times in a year

t: number of years to deposit or invest

PMT: additional deposit amount per period

For example:

Initial deposit of 50 million VND, additional 2 million per month, interest rate of 8%/year, for 3 years:

This formula consists of two parts, specifically:

Clause 1: The value of the initial deposit (50 million VND) after 3 years is: 50,000,000 × (1 + 0.08/12)^36 = 50,000,000 × 1.2702 ≈ 63,510,000 VND

Clause 2: The total value of additional deposits (2 million VND/month) and the interest on the additional deposit is: 2,000,000 × [((1 + 0.08/12)^36 - 1) / (0.08/12)] = 2,000,000 × [(1.2702 - 1) / 0.00667] = 2,000,000 × 40.53 ≈ 81,060,000 VND

→ Final total: 63,510,000 + 81,060,000 ≈144,570,000 VND.

It can be seen that the compounding frequency directly affects the profit. The larger n is (compounding more frequently, such as monthly instead of annually), the higher the profit, even though the difference is not too large. Understanding the compounding formula helps you choose the optimal form of savings or investment, effectively growing your capital over time.

3. 3 Practical applications of the compound interest formula

3.1. Bank savings

When saving at the bank, the interest can be automatically added to the principal after each term (month, quarter, year), forming natural compound interest. This form helps increase profits significantly over time without having to deposit additional capital.

3.2. Long-term securities investment

In stock or ETF investing, reinvested dividends are an indirect form of compounding. When dividends are used to buy more shares, the investor owns more shares, thereby multiplying the profits.

3.3. Pension funds, life insurance

Compound interest plays an important role in long-term financial products, such as pension funds, life insurance, or education savings plans. Participants make regular payments, and the payments grow steadily over many years using compound interest.

The compound interest formula can be applied in many situations.

4. 3 Important notes when applying compound interest

Compound interest can be very beneficial if applied correctly. However, to maximize efficiency and avoid risks, you need to keep in mind the following factors:

Nominal interest rate and real interest rate: Nominal interest rates are the bank's stated rates; real interest rates reflect returns after inflation. If inflation is higher than the interest rate, your money will lose value even if it increases in value.

Impact of deposit/investment time: The longer the time, the greater the power of compound interest. Investing early allows small amounts of money to grow significantly over time thanks to “compound interest.”

The risks of expecting high interest rates: High returns often come with high risks. Promises of unusual compound interest may be a sign of fraud. Choose a reputable, transparent investment channel that suits your financial capacity.

5. Fast savings deposit, preferential interest rate at SeABank

If you want to take advantage of the power of compound interest safely and effectively, saving at SeABank is a reliable choice. The bank offers a variety of flexible terms, competitive interest rates and quick account opening procedures in just a few minutes.

Customers can quickly own a savings account at SeABank

Customers can easily deposit savings online via the SeAMobile, SeANet applications or at the nearest transaction counter, with full utilities:

Track balances and interest in real time.

Automatic renewal upon maturity.

Enjoy preferential interest rates when depositing long terms or large amounts.

SeABank offers flexible savings products, competitive interest rates and automatic renewal features, helping customers take full advantage of the power of compound interest..

Learn about SeABank's interest rates and savings products on the official website www.seabank.com.vn or contact Hotline 1900 555 587 for detailed advice.

Southeast Asia Commercial Joint Stock Bank SeABank